Travel Insurance Essentials: Why You Need It and How to Choose the Right Plan

Travel Insurance Essentials: Why You Need It and How to Choose the Right Plan

Do You Need It and How to Choose the Right Plan

Introduction

Imagine this: You're on a dream vacation in Bali, enjoying the sun and surf, when suddenly, you slip on a wet surface and twist your ankle. A trip to the local hospital reveals a fracture, and your relaxing vacation becomes a stressful ordeal with mounting medical bills and the need to cut your trip short.

Or consider this statistic: According to the US Travel Insurance Association, one in six Americans has their travel plans impacted by medical conditions, natural disasters, or other unexpected events, underscoring the importance of having a safety net while traveling.

Travel insurance can be a crucial lifeline in such scenarios, offering financial protection and peace of mind. In this guide, we'll explore why travel insurance is essential when you need it and how to choose the right plan to ensure your trips remain as stress-free as possible.

Section 1: Understanding Travel Insurance

1.1 What is Travel Insurance?

Travel insurance is insurance coverage designed to protect travelers from unexpected events and financial losses before or during their trip. The primary purpose of travel insurance is to provide financial protection and support in case of unforeseen circumstances, ensuring that travelers can manage and mitigate potential risks associated with travel.

Types of Coverage

1. Trip Cancellation Insurance

Definition: This coverage reimburses you for non-refundable trip expenses if you need to cancel your trip for a covered reason.

Examples of Covered Reasons are illness, injury, death of a family member, natural disasters, or unforeseen events like jury duty or job loss.

Benefits: Protects your investment in prepaid travel arrangements such as flights, hotels, and tours.

2. Medical Insurance

Definition: Provides coverage for medical emergencies and healthcare costs incurred during your trip.

Examples of Coverage: Doctor visits, hospital stays, emergency surgeries, and medical evacuations.

Benefits: Essential for international travel, where your regular health insurance may not provide coverage.

3. Emergency Evacuation Insurance

Definition: Covers the cost of emergency medical evacuations to the nearest adequate medical facility or back home.

Examples of Coverage: Air ambulance, medically necessary repatriation, and transportation to a hospital.

Benefits: Ensures you receive appropriate medical care in case of severe illness or injury.

4. Baggage Insurance

Definition: Reimburses you for lost, stolen, or damaged baggage and personal items during your trip.

Examples of Coverage: Replacement of lost luggage, compensation for damaged items, and coverage for delayed baggage.

Benefits: Provides peace of mind and financial support if your belongings are compromised.

5. Trip Interruption Insurance

Definition: Covers the cost of returning home early due to an emergency and reimburses unused portions of your trip.

Examples of Coverage: Illness, injury, or death of a family member, natural disasters, or other unforeseen events requiring an early return.

Benefits: Helps manage additional travel expenses and minimizes financial losses from interrupted travel plans.

6. Accidental Death and Dismemberment Insurance (AD&D)

Definition: Provides financial compensation in case of accidental death or severe injury resulting in dismemberment during your trip.

Examples of Coverage: Accidental death, loss of limbs, or loss of sight due to an accident.

Benefits: Offers financial support to you or your beneficiaries in the event of a tragic accident.

7. Rental Car Insurance

Definition: Covers damage or theft of a rental car during your trip.

Examples of Coverage: Collision damage waiver, liability insurance, and repair reimbursement.

Benefits: Protects you from high out-of-pocket costs associated with rental car incidents.

8. Travel Delay Insurance

Definition: Reimburses you for additional expenses incurred due to travel delays.

Examples of Coverage: Meals, accommodations, and transportation costs resulting from flight delays, inclement weather, or other unforeseen events.

Benefits: Provides financial assistance and reduces the inconvenience of travel disruptions.

Understanding the various types of travel insurance coverage available can help you decide on the best plan for your needs. Each type of coverage addresses specific risks and offers different benefits, ensuring comprehensive protection for your travel adventures.

1.1A Is a critical point to consider. Just imagine this one key area to consider. The cost of Air Ambulance or Emergency Evacuation without Coverage. Remember, standard health insurance does not cover care when you are traveling.

The Cost of Air Ambulance or Emergency Evacuation Without Coverage

The cost of air ambulance or emergency evacuation can be extremely high without coverage, and the expenses can vary significantly depending on various factors such as location, distance, medical needs, and the type of aircraft used. Here are some general cost estimates to give you an idea of how expensive these services can be:

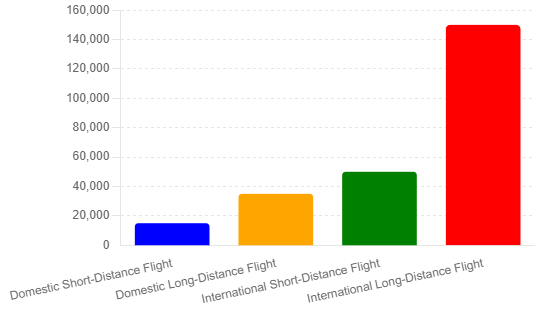

1. Domestic Air Ambulance Costs

Short-Distance Flights (Within the Same Country):

Cost: $10,000 to $25,000

Example: A flight within the United States from a remote area to a major city.

Long-Distance Flights (Across the Country):

Cost: $25,000 to $50,000

Example: A coast-to-coast flight within the United States.

2. International Air Ambulance Costs

Short-Distance International Flights:

Cost: $25,000 to $75,000

Example: A flight from the Caribbean to the United States.

Long-Distance International Flights:

Cost: $75,000 to $200,000 or more

Example: A flight from Asia or Africa to the United States or Europe.

Factors Influencing the Cost:

Distance: Longer distances increase fuel and operational costs.

Aircraft Type: The aircraft type (e.g., jet, turboprop, helicopter) affects the cost, with jets generally being more expensive.

Medical Equipment and Staff: Advanced medical equipment and specialized medical staff (e.g., doctors, nurses, paramedics) onboard increase costs.

Urgency: Emergency evacuations that require immediate response can incur higher costs.

Location and Accessibility: Remote or hard-to-reach locations may require additional logistics and higher fees.

Insurance Coverage: Without travel insurance, these costs must be paid out-of-pocket, making comprehensive travel insurance with emergency evacuation coverage essential for mitigating financial risk.

Example Scenarios:

Domestic Example:

A traveler in a remote area of Montana suffers a severe medical emergency and needs to be airlifted to a specialized hospital in Denver. The air ambulance flight could cost around $20,000 to $35,000.

International Example:

A traveler in Thailand suffers a serious injury and requires medical evacuation to their home country in the United States. The cost for such an international air ambulance flight could range from $100,000 to $150,000, depending on the specific medical needs and distance.

These high costs underscore the importance of having travel insurance that includes emergency evacuation coverage, providing travelers with peace of mind and financial protection against unforeseen medical emergencies abroad.

1.2 Why Do You Need Travel Insurance?

Common Scenarios Where Travel Insurance is Beneficial

1. Trip Cancellations or Interruptions:

Scenario: You book a non-refundable vacation package months in advance. Two weeks before your trip, a close family member falls seriously ill, and you need to cancel your plans.

Benefit: Trip cancellation insurance reimburses you for prepaid, non-refundable expenses, saving you from significant financial loss.

2. Medical Emergencies:

Scenario: While hiking in the Swiss Alps, you slip and fracture your leg, requiring immediate medical attention and hospitalization.

Benefit: Travel medical insurance covers your medical expenses, including hospital stays, doctor visits, and necessary surgeries, ensuring you receive proper care without worrying about the cost.

3. Lost or Delayed Baggage:

Scenario: Your checked luggage gets lost en route to your destination, leaving you without personal belongings for several days.

Benefit: Baggage insurance compensates you for lost items and provides funds to purchase essential items, such as clothing and toiletries, reducing the inconvenience and stress of lost luggage.

4. Travel Delays:

Scenario: A severe snowstorm delays your flight, forcing you to spend the night at the airport and incur additional expenses for food and accommodation.

Benefit: Travel delay insurance reimburses you for extra costs incurred due to the delay, helping you manage unexpected expenses.

5. Emergency Evacuations:

Scenario: While traveling in a remote area, you suffer a severe allergic reaction and require an emergency medical evacuation to the nearest suitable medical facility.

Benefit: Emergency evacuation insurance covers the cost of air ambulance services, ensuring you receive timely and appropriate medical care without incurring enormous out-of-pocket expenses.

6. Theft or Loss of Personal Items:

Scenario: Your wallet and passport are stolen while sightseeing in a foreign city.

Benefit: Travel insurance helps you replace stolen documents and provides emergency funds, helping you manage the situation with less stress.

Great Examples of Travel Insurance Saving the Day

Unexpected Illness:

Story: Jane was on a dream vacation in Southeast Asia when she contracted dengue fever. Her condition deteriorated quickly, and she needed immediate hospitalization and medical treatment. Fortunately, Jane had purchased travel insurance that covered medical emergencies. Her insurance covered the hospital bills and arranged for her medical evacuation back to her home country, where she received further treatment. Jane's travel insurance saved her from potentially overwhelming medical expenses and ensured she received the necessary care promptly.

Flight Cancellations Due to Natural Disasters:

Story: Mark and his family were on their way to the Caribbean for a long-awaited family reunion when a hurricane struck the region, causing widespread flight cancellations. Their trip was abruptly canceled, and they faced the prospect of losing thousands of dollars in non-refundable travel expenses. However, Mark had wisely invested in travel insurance with trip cancellation coverage. His insurance reimbursed them for their lost expenses, allowing the family to reschedule their trip without financial strain.

Lost Baggage:

Story: Emma's honeymoon started sourly when the airline lost her luggage containing all her clothing and essential items. With only the clothes on her back and no immediate solution in sight, Emma was distraught. Fortunately, she had purchased travel insurance that included baggage coverage. Her insurance provided funds to buy new clothes and essentials, allowing her to enjoy her honeymoon without constant worry about her lost luggage.

Travel Delays:

Story: John was traveling to attend an important business conference when his flight was delayed due to a mechanical issue. The delay caused him to miss his connecting flight and be stranded overnight in a different city. John's travel insurance covered the cost of his hotel stay and meals during the delay, ensuring he arrived at his destination rested and ready for the conference without incurring unexpected expenses.

Medical Emergency Abroad:

Story: During a safari in Kenya, Sarah experienced severe abdominal pain that required immediate medical attention. The local hospital diagnosed her with appendicitis and recommended surgery. Sarah's travel insurance covered her medical expenses, including the surgery and hospital stay, and even arranged a follow-up check-up once she returned home. The insurance coverage saved Sarah from significant medical bills and provided her with the necessary support during a distressing situation far from home.

These scenarios and personal stories illustrate travel insurance's invaluable protection, providing peace of mind and financial security in the face of unexpected events. Whether it's a medical emergency, a trip cancellation, or lost luggage, travel insurance ensures that travelers can focus on enjoying their journeys without the constant worry of unforeseen financial burdens.

Section 2: When to Get Travel Insurance

2.1 Factors to Consider

Type of Trip (Domestic vs. International):

Domestic Travel:

Consider travel insurance if your trip involves significant prepaid expenses (e.g., flights, accommodations, tours).

Valid for rental car insurance coverage, trip cancellations, and medical emergencies not covered by your primary health insurance.

International Travel:

Essential for covering medical emergencies, as your domestic health insurance may not provide coverage abroad.

Important for trip cancellation, interruption, baggage loss, and emergency evacuation coverage.

Duration of Travel:

Short Trips:

Travel insurance can still benefit short trips, especially if there are non-refundable expenses or potential health risks.

Evaluate the cost-to-benefit ratio based on the trip's length and your overall investment.

Long-Term Travel:

Highly recommended for extended trips, as the likelihood of encountering issues increases with the duration.

Consider comprehensive plans that cover various aspects, including health, baggage, and trip interruptions.

Health and Age of Travelers:

Health Conditions:

Travelers with pre-existing health conditions should look for policies covering medical issues arising from them.

Ensure the policy includes emergency medical and evacuation coverage.

Age Considerations:

Older travelers may face higher premiums but are at greater risk for medical emergencies.

Some policies are tailored specifically for senior travelers, offering extensive medical and evacuation coverage.

Destination-Specific Risks:

High-Risk Areas:

Travel insurance is crucial if you are traveling to areas prone to natural disasters, political instability, or high crime rates.

Policies may include coverage for trip cancellations due to advisories and emergencies specific to the destination.

Remote Locations:

Travel insurance is essential for remote destinations where medical facilities are limited.

Emergency evacuation coverage ensures you can be transported to a suitable medical facility.

2.2 Timing

When to Purchase Travel Insurance:

At the Time of Booking:

The best time to purchase travel insurance is when you deposit your initial trip.

The early purchase ensures trip cancellation and interruption coverage, protecting from the start.

Before the Final Payment:

Ensure you have coverage in place before making the final payment for your trip.

This timing provides a safety net in case unforeseen events arise before you complete your travel arrangements.

Importance of Coverage Start Date:

Immediate Coverage:

Policies typically begin covering trip cancellations from the day after purchase.

Medical and evacuation coverage usually starts from the trip's commencement date.

Waiting Periods and Exclusions:

Some policies may have waiting periods for specific coverages, such as pre-existing medical conditions.

Review the policy details to understand any exclusions or waiting periods that may apply.

By considering these factors and timing your purchase appropriately, you can ensure that your travel insurance provides comprehensive protection tailored to your specific needs and travel plans. Proper planning and timely acquisition of travel insurance can save you from potential financial losses and stress, allowing you to enjoy your trip with peace of mind.

Section 3: Choosing the Right Travel Insurance Plan

3.1 Assess Your Needs

Identify Key Coverage Areas:

Trip Cancellation and Interruption:

Essential if you have significant prepaid, non-refundable expenses.

This is important for multiple flights, hotels, and tours.

Medical Coverage:

Crucial for travelers where health insurance may not apply.

Look for plans covering emergency medical treatment, hospitalization, and evacuation.

Baggage and Personal Belongings:

Beneficial if you are carrying valuable items or have tight travel schedules.

Coverage for lost, stolen, or damaged baggage and personal items.

Travel Delays and Missed Connections:

Important for trips with tight schedules or multiple connections.

Provides compensation for additional expenses incurred due to delays.

Adventure and Sports Activities:

Necessary if you plan on engaging in high-risk activities (e.g., skiing, scuba diving).

Ensure the plan covers injuries or incidents related to these activities.

Prioritize Coverage Types:

Comprehensive Plans:

Offer broad coverage, including trip cancellation, medical emergencies, baggage, and more.

Ideal for extensive or high-cost trips.

Specialized Plans:

Tailored for specific needs, such as medical-only coverage or adventure sports.

Suitable for travelers with focused requirements.

3.2 Comparing Plans

Key Features to Look For:

Coverage Limits:

Check maximum payout limits for each coverage type (e.g., medical, trip cancellation).

Ensure the limits are sufficient for your potential needs.

Deductibles and Co-Pays:

Understand the amount you need to pay out-of-pocket before coverage kicks in.

Compare deductibles across different plans to find the most affordable option.

Policy Exclusions:

Review what is not covered, such as pre-existing conditions, certain activities, or specific destinations.

Choose a plan with the fewest exclusions relevant to your travel plans.

Tips for Reading the Fine Print:

Understand Terminology:

Familiarize yourself with insurance terms like "pre-existing conditions," "primary/secondary coverage," and "medical evacuation."

Check Claim Procedures:

Look into how claims are filed, the required documentation, and the process timeline.

Ensure the insurer has a straightforward and efficient claims process.

Cancellation Policies:

Understand under what circumstances you can cancel the policy and receive a refund.

Some policies offer a "free look" period for cancellations within a specified timeframe.

Using Comparison Websites:

Aggregators:

Use sites like InsureMyTrip, Squaremouth, and TravelInsurance.com to compare multiple plans side-by-side.

Enter trip details to get tailored quotes and coverage options.

Customer Reviews:

Read reviews and ratings from other travelers to gauge the reliability and satisfaction with the insurer.

Pay attention to comments about claims processing and customer service.

3.3 Cost vs. Coverage

Balancing Premium Costs with Coverage Benefits:

Budget Considerations:

Determine how much you are willing to spend on travel insurance based on your trip's value and risk factors.

Compare premiums to find a balance between affordability and comprehensive coverage.

Coverage Value:

Evaluate whether the coverage provided justifies the premium cost.

Opt for plans that offer essential protections without unnecessary extras.

Understanding Deductibles and Limits:

Deductibles:

A higher deductible can lower your premium but ensure you can afford it.

Compare deductible options and choose a plan that offers a manageable balance.

Coverage Limits:

Ensure the plan's coverage limits meet your needs, especially for medical expenses and evacuation costs.

Higher limits may come with higher premiums but provide better protection.

By carefully assessing your needs, comparing plans, and balancing costs with coverage benefits, you can select the right travel insurance plan to protect your trip and provide peace of mind. Choosing the appropriate plan ensures you are well-prepared for any unexpected events during your travels.

Also, if you are busy, overwhelmed, and need so much support, check out our sister site, Think Healthcare Solutions.

Section 4: Fixing Common Travel Insurance Issues

4.1 Common Problems and Solutions

Claim Denials:

Problem: Your claim is denied due to technical issues or a lack of proper documentation.

Solution:

Review the policy thoroughly before purchasing to understand coverage and exclusions. When filing a claim, ensure you provide all required documentation, such as receipts, medical reports, and proof of loss. If denied, request a detailed explanation and consider appealing the decision with additional supporting evidence.

Policy Misunderstandings:

Problem: Misinterpreting the policy terms and finding out too late that something needs to be covered.

Solution:

Take time to read the entire policy document, including the fine print. If anything is unclear, contact the insurance provider for clarification. Use resources like FAQs and customer service to understand what is covered and what isn't.

Pre-Existing Condition Exclusions:

Problem: Your medical claim is denied because it involves a pre-existing condition.

Solution:

Look for policies that offer coverage for pre-existing conditions. Many insurers have a "look-back" period to determine if a condition is pre-existing. Please disclose all relevant medical history when purchasing the policy and check if a waiver for pre-existing conditions is available.

Coverage Gaps:

Problem: Discovering that your travel insurance only covers certain activities or destinations.

Solution:

Ensure the policy you choose covers all planned activities and destinations. If engaging in high-risk activities, select a plan that explicitly includes those activities. Verify the geographic coverage area and any travel advisories that might affect your coverage.

Customer Service Issues:

Problem: Difficulty in reaching customer service or receiving unsatisfactory support.

Solution:

Research customer service reviews before purchasing a policy. Choose an insurer known for responsive and helpful customer service. Keep all communication records and escalate unresolved issues to a higher level if necessary.

4.2 Tips for Smooth Claims

Documentation Requirements:

Tip: Keep all receipts, booking confirmations, medical reports, police reports (if applicable), and other relevant documents. Organize them in a folder or digitally for easy access when filing a claim.

Filing Claims Promptly and Accurately:

Tip: Submit your claim as soon as possible after an incident occurs. Ensure all forms are filled out completely and accurately. Double-check for any missing information or documentation before submission.

Keeping Thorough Records:

Tip: Maintain a detailed record of all interactions with the insurance company, including dates, names of representatives, and summary of discussions, which can be crucial if any issues arise during the claims process.

Contacting Customer Service for Resolutions:

Tip: If you encounter any problems, contact the insurance provider's customer service immediately. Be polite but firm when explaining your issue. If the initial representative cannot resolve the problem, request to speak with a supervisor or higher-level representative.

Appealing Denied Claims:

Tip: If your claim is denied, request a detailed written explanation. Gather any additional evidence or documentation that supports your case and file an appeal. Consider seeking assistance from a travel insurance advocate if needed.

By understanding common issues and following these tips, you can navigate the travel insurance process more effectively, ensuring you receive the coverage and support you need when unexpected travel events occur. Proper preparation and proactive travel insurance management can mitigate potential problems and provide a smoother experience.

Section 5: Expert Tips and Recommendations

5.1 Advice from Travel Experts

Interviews or Quotes from Travel Bloggers and Industry Professionals:

Travel Bloggers:

Jane, Travel Blogger:"I always recommend getting travel insurance, especially for international trips. Knowing you're covered if something goes wrong is worth the peace of mind. Look for plans that include emergency medical evacuation and trip interruption. Trust me, you don't want to be stuck abroad without these coverages."

John, Adventure Travel Blogger:"For adventure travelers, it's crucial to choose a plan that covers activities like hiking, skiing, or scuba diving. Read the policy carefully to ensure your activities are included. I once had a mishap while rock climbing in the Alps, and my travel insurance covered my medical bills and the cost of getting me back home."

Industry Professionals:

Sarah Johnson, Travel Insurance Agent:"When selecting travel insurance, always compare different policies and their coverage details. Don't just go for the cheapest option; ensure it meets your needs. Look at the policy's exclusions and limitations to avoid surprises later."

Michael, Travel Consultant:"For family trips, consider a comprehensive family plan that covers all members. It's often more cost-effective and ensures everyone is protected. Also, check if the policy offers 24/7 emergency assistance, which can be a lifesaver in a different time zone."

5.2 Final Checklist

Summary of Key Points:

Assess Your Needs:

Identify the essential coverages for your trip (e.g., medical, trip cancellation, baggage).

Consider the type of trip, duration, health conditions, and destination-specific risks.

Compare Plans:

Look for policies with sufficient coverage limits, reasonable deductibles, and minimal exclusions.

Use comparison websites and read customer reviews to make an informed decision.

Purchase Timing:

Buy travel insurance when you deposit your initial trip to ensure comprehensive coverage.

Ensure the policy covers your entire trip duration and consider any waiting periods for pre-existing conditions.

Understand the Policy:

Read the policy documents thoroughly, including the fine print.

Contact the insurer for clarification on any unclear terms or conditions.

Document Everything:

Keep all receipts, medical reports, and correspondence related to your trip and any claims.

File claims promptly and accurately, following the insurer's procedures.

Quick Reference Guide for Choosing and Using Travel Insurance:

Determine Coverage Needs:

Medical emergencies, trip cancellation, baggage loss, travel delays, adventure activities.

Research and Compare:

Use tools like InsureMyTrip, Squaremouth, and TravelInsurance.com.

Review the insurer's reputation for customer service and claims handling.

Purchase Early:

Get insurance immediately after booking your trip.

Ensure coverage starts from the booking date and covers cancellations.

Review Policy Details:

Check coverage limits, deductibles, and exclusions.

Understand the claims process and required documentation.

Keep Records:

Maintain organized documentation for claims.

Contact customer service promptly for any issues or questions.

By following these expert tips and using the final checklist, you can confidently choose the right travel insurance plan for your needs and ensure you're well-prepared for unexpected travel events. This preparation will allow you to focus on enjoying your trip with peace of mind.

Conclusion

Recap: Summary of the Importance of Travel Insurance

Travel insurance is essential to any travel plan, offering a safety net against a wide range of unforeseen events. Travel insurance provides financial protection and peace of mind, from trip cancellations and medical emergencies to lost baggage and travel delays.

It ensures that you are prepared for the unexpected, whether you are traveling domestically or internationally. Understanding the various types of coverage, assessing your specific needs, and selecting the right plan can significantly affect how well you handle potential disruptions during your trip. By investing in travel insurance, you protect yourself and your loved ones from substantial financial loss and stress, allowing you to enjoy your travels confidently.

Call to Action:

Evaluating your travel insurance needs is crucial in planning a safe and enjoyable trip. Here are a few tips to get started:

Assess Your Trip Details:

Consider the nature of your trip, the destination, the duration, and any planned activities.

Identify the key risks and coverage areas most important for your journey.

Compare Policies:

Explore different plans using comparison websites like InsureMyTrip,Squaremouth, and TravelInsurance.com.

Look for policies that offer comprehensive coverage and align with your specific needs.

Read the Fine Print:

Thoroughly review the policy details, including coverage limits, exclusions, and claims procedures.

Contact the insurance provider for any clarifications or questions.

Purchase Early:

Buy your travel insurance when you book your trip to ensure complete coverage.

Consider annual travel insurance if you travel frequently, as it can be more cost-effective.

By taking these steps, you can choose a travel insurance plan that best fits your needs, providing the protection and support you need to travel with peace of mind. Don't wait until it's too late—evaluate your travel insurance needs today and decide to safeguard your travel experiences.

Download the Travel Insurance Cheat Sheet to ensure you choose the right travel insurance plan and travel with peace of mind!

© thinksavvytravel.com